A fair system to balance bankrupt and creditor rights.

A bankrupt’s income is assessed during their bankruptcy period (usually three years but can be extended) to determine whether they are liable to contribute some of that income to their bankruptcy administration. The premise being that if the person was not bankrupt, they would be using some of that income to pay off their debts. The contribution system seeks to compensate creditors while allowing a bankrupt to maintain a fair standard of living. The formula to calculate whether a bankrupt is required to contribute income is:

Assessed income – actual income threshold amount ÷ 2.

The law also sets out:

The law also sets out:- what is included as income

- what deductions are allowed (income less deductions = ‘assessed income’)

- what threshold is used based on number of dependants (i.e. the ‘actual income threshold amount’)

- how the liability is paid

- additional protections for the bankrupt and the bankruptcy trustee.

Section 139L (b) of the Bankruptcy Act 1966 sets out what is included as income. Income typically includes salary and wages, and profit from operating a business as set out in tax law. However, it may also include income that may not be taxable. Among others, income for the purposes of the calculation includes fringe benefits (click here to read more), loans received, superannuation payment in excess of 10 percent, some allowances not expended on work-related expenses, and tax refunds earned after the date the bankruptcy commenced.

The income is then reduced by allowable deductions. The standard deductions are income tax actually paid and the Medicare levy. Other deductions can include child support payments if paid under a Family Law Act 1975 maintenance agreement or order. Also, certain business expenses are deductable under section 139N of the Bankruptcy Act.

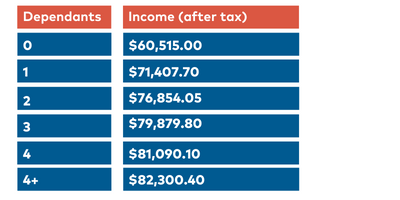

This results in the ‘assessed income amount’. Then the appropriate threshold must be determined. Twice a year[1], the Australian Financial Security Authority (AFSA) indexes the after-tax thresholds that apply to bankrupts in line with CPI and base pension rates in conjunction with how many dependants a bankrupt has in each year of their bankruptcy.

Currently, those amounts are:

So, on the basis above, currently anyone earning less than $60,515 after tax per year without dependants, will not be required to make an income contribution into their bankruptcy. However, if the assessed income amount is greater than the applicable threshold in the table above, half of the difference between these two amounts is required to be paid to the bankruptcy trustee.

Bankrupts are given notice of how the income contribution amount payable—and of course, how they were calculated. These income contributions become a legal obligation that becomes a new debt that survives beyond being discharged from bankruptcy. So that bankrupts can plan and budget, most bankruptcy trustees will set out a payment plan for the liability to be paid over time, usually monthly or in line with the bankrupt’s pay/income cycle.

Bankrupts and bankruptcy trustees have many mechanisms available to them to ensure the process is accurate and adhered to. These include:

- The bankruptcy trustee being able to investigate income.

- The bankruptcy trustee making a determination on behalf of the bankrupt when information is not forthcoming or timely.

- The bankruptcy trustee being able to issue notices to employers or other people that owe the bankrupt money to garnishee those monies (i.e. order third parties to withhold monies owing to the bankrupt and redirect the monies to the bankruptcy trustee).

- The bankruptcy trustee being able to use the ‘supervised account regime’ to monitor withdrawals.

- The bankruptcy trustee being able to extend the bankruptcy period and deny permission for overseas travel.

- The bankrupt being able to get an adjustment on the previous year based on actual income (favourable if less than the amount assessed).

- The bankrupt being entitled to have their liability reduced if faced with financial hardship (click here to read more).

- The bankrupt being able to get an assessment reviewed (within 60 days) by the Inspector-General.

- The bankrupt being able to get the Inspector-General’s decision reviewed by the Administrative Appeals Tribunal.

All this information and more, is available in our Guide to Personal Insolvency (click here).

The income contribution regime seeks to strike a balance between providing the bankrupt relief from their debts and allowing creditors some benefit during the bankruptcy from the bankrupt’s ongoing income.

Your local Worrells partner is here to help and will explain all the implications of bankruptcy along with any alternative solutions available.

Related articles:

Income contributions in bankruptcy: fringe benefits from a spouse

Enforcing income contributions in bankruptcy

Bankruptcy income assessments: hardship cases

[1] Updated on 20 March and 20 September each year.