How liquidation discussions can quickly turn into bankruptcy discussions.

In our initial meetings with SME company directors, it is becoming increasingly common for a discussion regarding the company's financial position and a possible liquidation, turning into a discussion about a personal insolvency for the director themselves. Some directors may think they are protected by the ‘corporate veil’ regarding their personal assets. However, there are limitations and many ways the veil can be pierced.

While our regulators prohibit us providing advice to a person regarding their company and their personal financial position, it is a difficult line to follow given the personal affairs of directors in small businesses are intrinsically linked to their company. We’re adept at navigating these discussions so that clients get the information they need while knowing that no ethical boundaries are crossed.

When we meet with the company directors who operate a small business the general discussion starts with obtaining some company history and background before discussing its assets and liabilities.

In many cases there are little to no company assets remaining. Therefore, the discussion can be quite short. Conversely, the discussion regarding its liabilities can become lengthy.

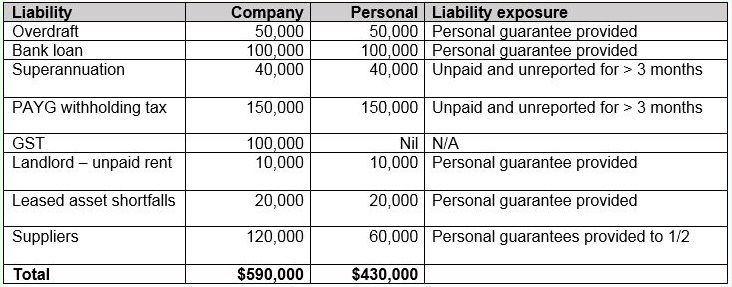

The conversation will generally start with bank facilities, then taxation obligations and superannuation, followed by lease liabilities and trade creditors. It can quickly become apparent that is it not just the company that may be facing financial difficulty.

Here’s an example of a recent matter with details of the company’s debts and the extent that the director was personally liable for:

To make matters worse, once the company accountant supplied the company’s financial statements, there was a director’s debit loan of $150,000. So, in addition to the $430,000 in liabilities that the director is personally liable for, the director is also indebted to the company for $150,000!As the above shows, the director is personally liable for a significant proportion of the company’s liabilities.

The question for the director then becomes whether there is any point initiating a voluntary winding-up of the company? As minimal assets are available, the director would need to contribute funds to pay for the liquidation. Certainly, liquidating the company would limit any further potential for insolvent trading, restrict any further amounts that may be lost by creditors and allow for an orderly closure of the company. However, as the director has limited funds and is facing personal claims totalling in excess of $430,000, this may not be possible.

Generally, in circumstances such as the above, the director must decide: initiate a voluntary liquidation or let the company die a slow death, either through the Australian Securities and Investments Commission (ASIC) initiating a company deregistration or letting a creditor proceed with a winding-up, most commonly being the Australian Taxation Office (ATO). Whichever comes first. In the case of a winding-up, the lack of any default “government liquidator” means the liquidator who provides a consent to act to the petitioning creditor will be left with a company with no assets and a director who may well be bankrupt as a result of personal liabilities associated with the company.

With GST being proposed to be added to the list of liabilities a company director is personally liable for (click here for more info), it raises the question—is there a corporate veil anymore for SME directors?

Your local Worrells partner is available as confidential and complimentary to discuss any financial challenges your clients may be experiencing.

Related article:

The heavyweight battle: Sole Trader v Company