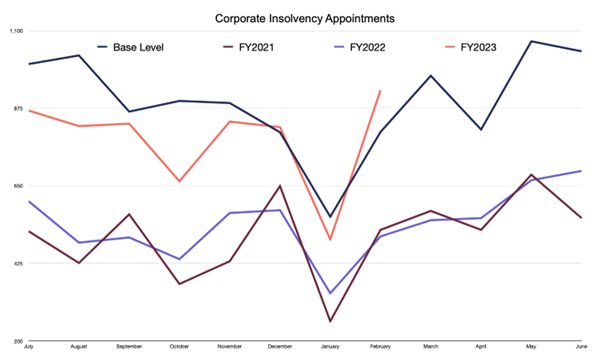

Corporate insolvency appointments at highest rate since November 2020.

2023 is promising to be a volatile and interesting year, with a lot of uncertainty, especially as we look forward to the latter half of 2023.

Corporate insolvencies

Corporate insolvency appointments started the year at a low point, which is normal as January is always the slowest month for corporate insolvency appointments. However, appointments showed significant growth in February with 927 corporate insolvencies. This is the highest monthly appointments since November 2020. Corporate insolvency appointments have now been above the long-term average in two out of the last three months.

We are starting to see clear indicators that corporate stress levels are rising and, and as a result, we expect corporate insolvency levels to remain above the long-term average for rest of this year.

Additionally, we are starting to see a rise in the number of winding up applications being filed, and debt collection activity by the Australian Taxation Office (ATO). Both factors will flow through to more corporate insolvencies in the second half of 2023.

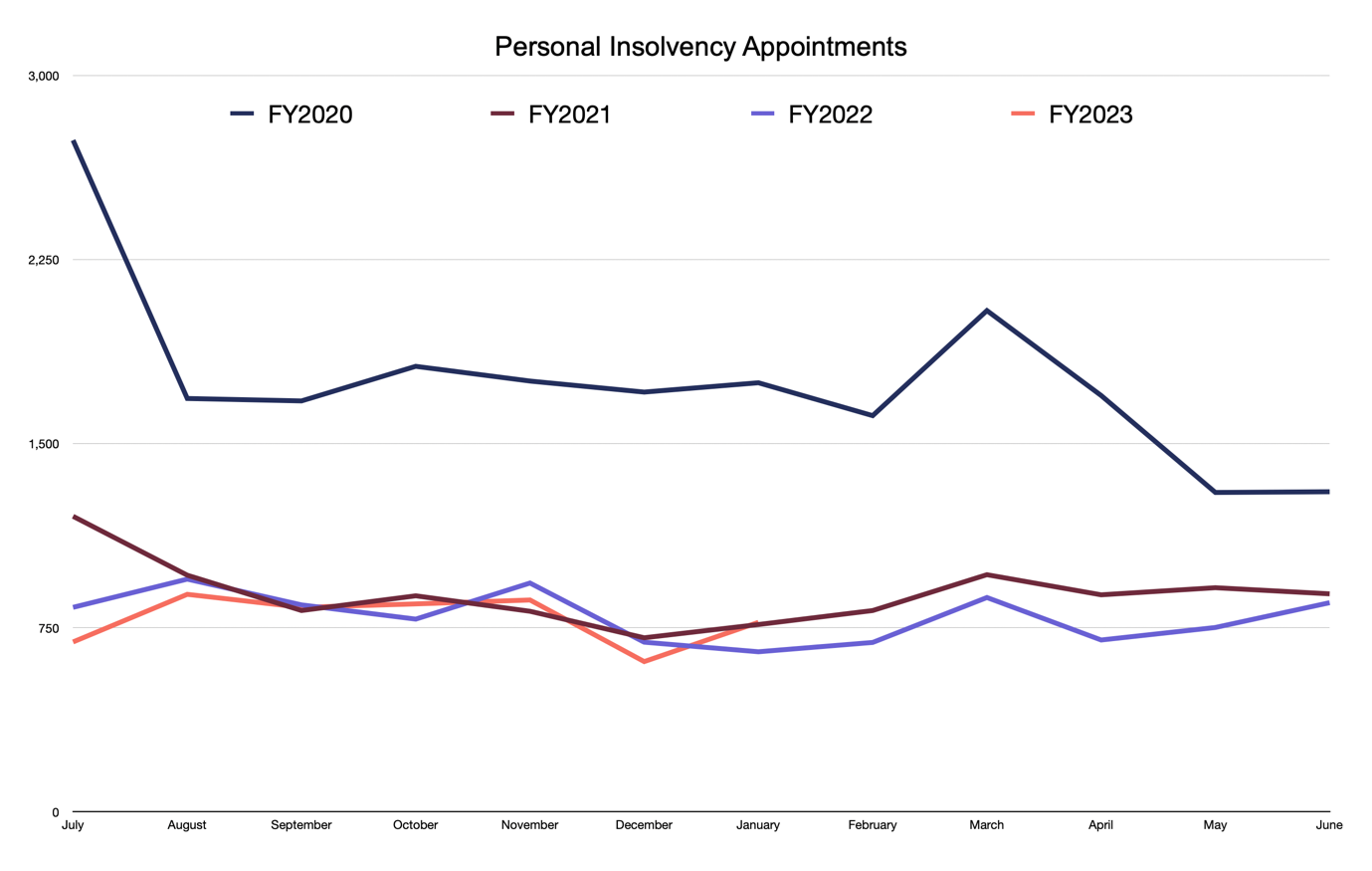

Personal insolvencies

Personal insolvency appointments have remained at or near record lows through the last two years and 2023 has started much the same, despite recent increases in corporate insolvencies.

I don’t expect we will see any significant increase in personal insolvency numbers until unemployment numbers start to rise. Over the last two years households have moved from an economy dominated by government stimulus and ultra-cheap finance to one of essentially full employment. Both cheap (or free money in the case of stimulus) and low unemployment have suppressed personal insolvency appointments over the last two years and will continue to do so if these factors persist.

What will drive insolvencies?

There are three key factors that are likely to drive a move to above trend insolvency appointments in the later half of this year:

Interest rates.

ATO debt collection.

Falling real wages.

Interest rates

Interest rates are likely to continue to rise for the next few months, and to stay high for an extended period. This will place pressure on both households, where it hits the bottom line and impacts their spending, and businesses, where is makes finance both more expensive and more difficult to get.

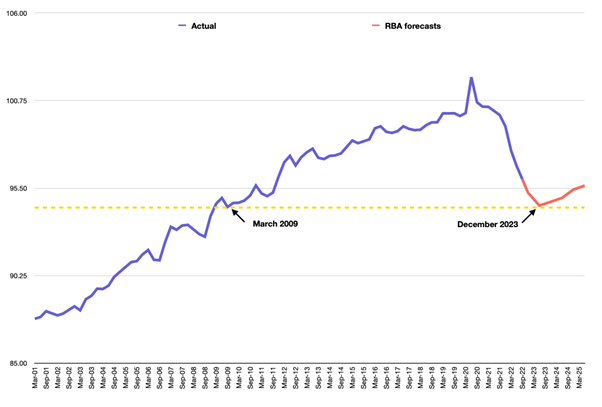

We don’t know how high interest rates will ultimately have to go to tame inflation, but it’s a fair bet that they will finish up higher than current expectations. The only real certainty we’ve seen over this RBA hiking cycle is that interest rate expectations have continued to increase as interest rates have. We’ve been two or three further rate increases away from peak rates since rates were at 1.5%.

When business owners and households are making their budgets and considering what to spend and what to borrow, I would be very careful about ‘hanging your hat’ on any forecasts of the peak cash rate. While the inflation rate has started to trend downwards, and we are likely closer to peak rates that we were six months ago, there are still credible scenarios where the RBA is forced to take interest rates above current estimates of a 4.1% peak rate.

ATO debt collection

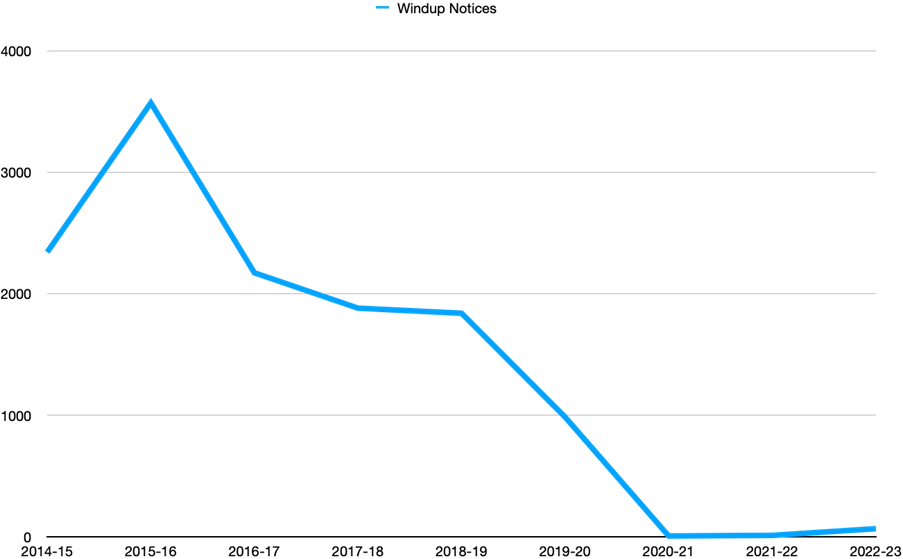

While there has been much commentary over the last nine months about the ATO’s return to debt collection activity, it’s important to keep in perspective how little they have done so far, and nothing highlights that point better than the chart below showing historical ATO winding up activity.

Winding up companies is the last of the ATO’s debt collection tools, the one they turn to when nothing else has worked, and ATO winding up activity remains minuscule. Pre-pandemic, the ATO averaged a little over 2,000 wind-up applications per year. So far this financial year, it has only filed 65.

What this means is there is a lot of pent up ‘demand’ for ATO winding up applications and these are bound to happen sooner or later. We‘ve talked many times about the significant small business debt that the ATO has accrued during the COVID period. All this debt must be collected eventually, and with response rates to softer ATO campaign currently sitting around 33%, there are an awful lot of small businesses where the ATO may be forced to resort to firmer action over the coming years.

Falling real wages

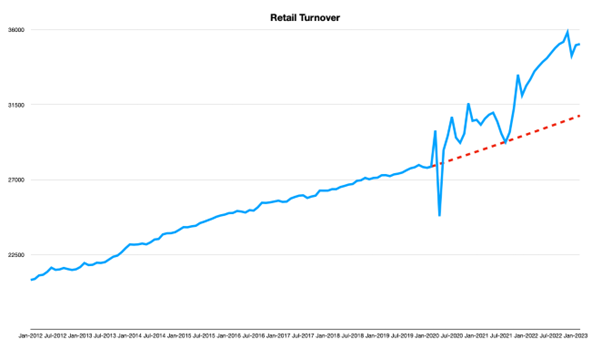

One of the key factors that has kept business confidence high and allowed many businesses to put off an insolvency appointment has been high consumer spending, which has remained well above trend since lockdowns ended in 2021.

This above trend spending cannot last as real wages have been falling at a historic rate. Real wages represent the buying power of household incomes, and it is impossible for household consumption to continue to rise indefinitely while real household income continues to fall. While households have maintained spending by drawing on savings, borrowing, and stretching household budgets, none of these factors are sustainable and a slowdown is inevitable.

When the slowdown gets here, businesses that were just getting by will suddenly find themselves short of cash flow and this will flow through the increased corporate insolvencies. We will also see overstretched households turn to (or be forced into) personal insolvencies as times get more difficult.

Picking when this turn will happen is a much harder task as various commentators and economists have been predicting a downturn in consumer spending since mid-last year. However, spending has remained surprisingly resilient. While spending data looks like it may be starting to plateau over the last few months, I'm conscious of the experience in the USA, where retail spending slowed in mid-2022, but has proven surprisingly resistant to an actual downturn.

[i] Australian Securities and Investments Commission Insolvency Statistics Series 2 - https://asic.gov.au/regulatory-resources/find-a-document/statistics/insolvency-statistics/insolvency-statistics-current/

[ii] AFSA Monthly Personal Insolvency Statistics - https://www.afsa.gov.au/about-us/statistics/monthly-personal-insolvency-statistics

[iii] Australian Bureau of Statistics Monthly Consumer Price Index indicator - https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/monthly-consumer-price-index-indicator/feb-2023

[iv] Manually collected each month via ASIC Published notices website: https://publishednotices.asic.gov.au/

[v] Australian Bureau of Statistics, Retail Trade Australia - https://www.abs.gov.au/statistics/industry/retail-and-wholesale-trade/retail-trade-australia/feb-2023

[vi] Australian Bureau of Statistics, Wage Price Index - https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/wage-price-index-australia/latest-release

.jpeg?auto=format,compress&cs=tinysrgb&fit=crop&crop=focalpoint&fp-x=0.50&fp-y=0.50&fp-y=0.1&w=800&h=480&q=25&blur=5&sat=-100)

.jpg?auto=format,compress&cs=tinysrgb&fit=crop&crop=focalpoint&fp-x=0.50&fp-y=0.50&fp-y=0.1&w=800&h=480&q=25&blur=5&sat=-100)