Business failure is rarely caused by a single mistake.

Most people might think that poor economic conditions are the main reason for failure. However, based on liquidator data, the economic conditions cause only 8% of external administrator appointments, which leads to the question: what caused the other 92% of companies to fail?

Business failures are usually the result of factors within the owners’ control. By keeping these in mind, owners can (hopefully) make their business more profitable and avoid joining the approximately 9,000 insolvent companies that were placed into liquidation in the 2025 financial year.

What does the data say?

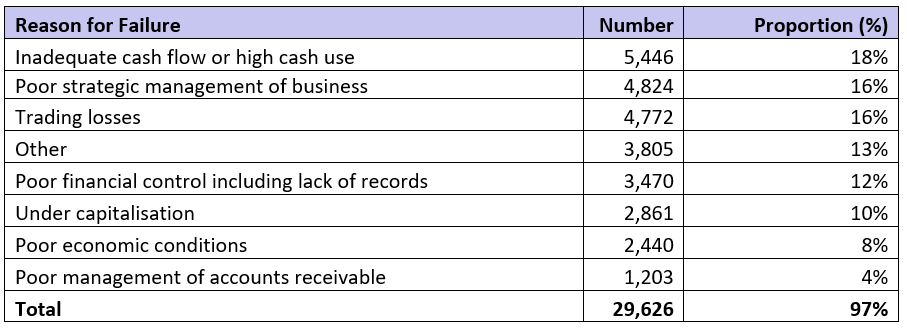

Based on data reported by external administrators to ASIC, 97% of businesses fail due to at least one of the following reasons in the 2025 FY:

Let’s take a look at each of these reasons:

1) Inadequate Cash Flow or High Cash Use (18%)

The saying “cash is king” is as true today as it was 100 years ago, assuming it was referring to cash flow forecasts. Cash flow refers to the timing and sufficiency of funds coming in versus funds going out. A business can be profitable “on paper,” yet still fail if it cannot pay debts when they fall due. Insolvency guidance highlights liquidity stress (e.g., liquidity ratios below 1, unpaid creditors outside trading terms, cash of delivery supplier demands) as classic warning signs that cash flow is failing.

Increases in work in progress (WIP) and accounts receivable (AR) on the balance sheet are great and may result in an accounting profit. However, if the business is not converting WIP and AR to cash, it may mean that its incurring expenses that are due in the present while the funds from work completed may be delayed. Even a profitable business could be insolvent in this case, as the business cannot pay its debts as and when they fall due.

2) Poor Strategic Management of the Business (16%)

In my experience, poor strategic management is usually reported where the business may have been viable, but there was a breakdown in the execution of the strategy. This can involve:

Misallocation of resources: businesses should have a clear understanding of what is most profitable to them.

Weak risk management and controls: an example is when quoting/tendering, the business is not pricing in risks adequately.

Inorganic growth: higher revenue does not always mean higher profits. Businesses may take on work that is unprofitable.

Poor business decision making: business owners can procrastinate making decisions or stick their hands in the sand. Not making a decision can be worse than making the wrong decision.

The unfortunate reality for directors is that there is no crystal ball. Owners make decisions in the dark, based on the information that they have available at the time. Sometimes, when external administrators investigate reasons for failure though, some decisions appear to be illogical in hindsight. The Corporations Act 2001 recognises that directors can only make decisions based on the information at hand. Section 180(2) has a specific carve-out for the business judgement rule.

Section 180(2) provides a safe harbour so that a director who makes a business judgment is taken to have met the duty of care and diligence if the decision is made in good faith for a proper purpose, without a material personal interest, and on an appropriately informed basis. The director must also rationally believe the judgment is in the best interests of the corporation, meaning courts will not second‑guess honest commercial decisions with hindsight.

3) Trading Losses (16%)

Trading losses occur when a business trades with costs greater than revenue. On their own, losses do not always equal insolvency (borrowing power, overdrafts, and related party capital are all taken into consideration when assessing insolvent trading) however, insolvency risk rises sharply when losses are paired with insufficient working capital or an inability to refinance. Insolvency indicators explicitly list continuing losses as a key warning sign and note that prolonged losses will eventually exhaust a business’s working capital.

If your business is trading at a loss, you need a plan, forecasts, and a timeframe for when it can be expected to trade at a profit. If the business cannot fund those trading losses, then it may be trading insolvently. In which case, you should consider speaking to an insolvency professional (like Worrells).

4) Poor Financial Control (Including Lack of Records) (12%)

In poor strategic management, I touched upon a business’s ability to make decisions based on the information it has available. Poor financial controls result in directors not seeing problems early and responding decisively. Insolvency practice and law-linked guidance recognise that an inability to produce timely and accurate financial information is itself an indicator of insolvency risk and correlates with financial distress.

If a business wants to restructure, one of the first questions I ask is whether the business is or can be profitable. If the business has poor records, the director often cannot answer that simple question.

5) Under-capitalisation (10%)

Under-capitalisation is reported when:

the business does not have enough funding to sustain operations obligations through volatility (start-up ramp, seasonality, shocks, wet weather, slow-paying debtors, etc.).

the business is over-reliant on debt for funding. The result of loans, hire purchase agreements, novated leases, and other instruments means that the business has a high monthly commitment to fixed monthly expenses. In addition, for equipment and vehicles, their value is at the mercy of the market, and they may quickly be worth a lot less than the finance owed on them during the first few years after purchasing.

The core of a business can be profitable, but if it is carrying and servicing high-interest debt facilities, then it may be incurring losses each year. This is a scenario where the business could benefit from a formal restructure to reduce the debt it carries.

6) Poor Economic Conditions (8%)

Most readers may be surprised that poor economic conditions were only attributable to business failure in 8% of cases in the 2025 financial year.

Economic downturns change customer demand, supplier availability and cost, credit availability, and default risk. Economic downturns typically bring declines in sales and profits, tighter credit, and increasing unpaid invoices (bad debtors causing a domino effect) as liquidity problems cascade through supply chains.

Perhaps the reason economic conditions appear to account for a relatively small share of failures is that Australia has experienced few broad-based recessions in recent decades. Under the commonly used “technical recession” definition (two consecutive quarters of negative real GDP growth), the RBA notes Australia went 29 years without a technical recession after the early‑1990s downturn.

Australia’s most recent technical recession was tied to the COVID‑19 shock, when GDP fell 0.3% in the March quarter 2020 and then 7.0% in the June quarter 2020. The government supported SMEs to such a large extent that, rather than see corporate insolvencies rise as a result of the recession, there was a large decrease in the number of corporate failures.

7) Poor Management of Accounts Receivable (AR) (4%)

Accounts receivable is where “revenue” becomes “cash.” Poor AR management (weak credit policies, slow invoicing, poor collections discipline, unresolved disputes) is a direct driver of cash-flow failure.

When a business is invoicing but not collecting it is essentially undertaking the work or supplying a good, still incurring operating costs without being paid.

Over the years, I have heard many stories of large businesses or organisations using their market power to demand long payment terms from their suppliers. Australia’s Payment Times Reporting Scheme was created specifically because long and late payment times place pressure on small businesses.

8) “Other” (13%)

Other is the catch-all category. Business failures aren’t always due to business issues. Some common examples of other reasons for failure:

Relationship breakdown between directors and/or business owners.

Business owner’s health issues

The reality is that, despite using a corporate shell, for most small businesses, the health of the business is directly related to the Director’s circumstances, including:

Personal relationships

Mental health

Physical health

Knowledge and competence

Further reading:

Stepping down to stay compliant | Worrells

The hidden cost of debt | Worrells

Turning around a sinking business

The data is clear: most business failures are not sudden or unavoidable events driven by the economy, but the cumulative result of issues that sit largely within an owner’s control. Cash‑flow stress, poor strategic execution, trading losses, weak financial reporting, and under‑capitalisation consistently appear as the primary drivers of insolvency, while broader economic conditions play a comparatively minor role. These factors rarely emerge overnight; they develop gradually, often accompanied by warning signs that go unaddressed for too long.

For directors, the key takeaway is not that failure is inevitable, but that it is often preventable. Timely access to accurate financial information, disciplined cash‑flow management, sound decision‑making, and a willingness to confront problems early can materially improve outcomes. When challenges do arise, seeking advice sooner rather than later can preserve options, protect directors, and in some cases save the business altogether. Insolvency is rarely a single moment in time; it is a process, and understanding its common causes is the first step in avoiding it.

If your business is no longer profitable or is drowning in debt, you still have options. A formal restructure can stabilise cash flow, reduce unsustainable debt, and give the business the breathing room it needs to recover. Worrells with owners and directors to assess viability, develop a practical restructuring plan, and implement formal solutions that protect the business while addressing creditor pressure. The earlier you act, the more options you have. If the warning signs are appearing, now is the time to get professional advice and take control of the outcome.